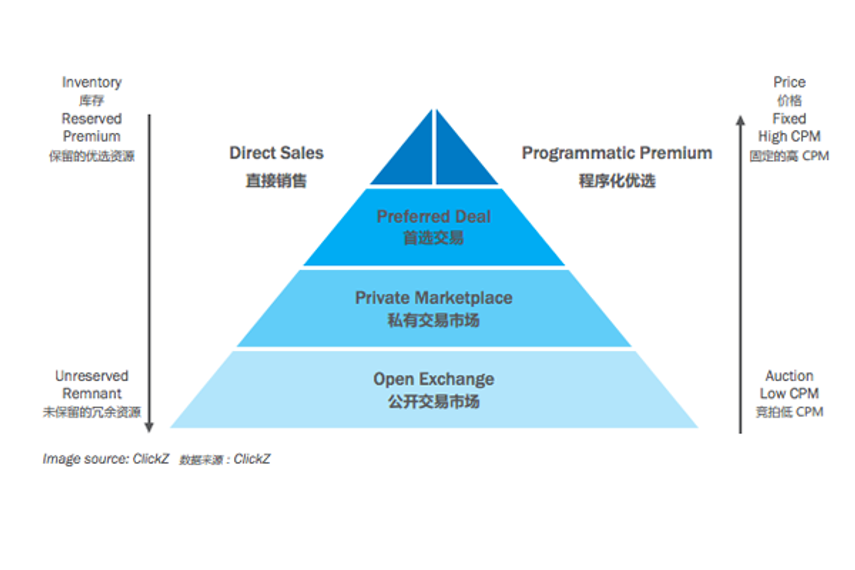

China's programmatic pyramid (pictured right, click here for enlarged view)

China's rapid shift away from traditional advertising, as well as factors unique to China, such as the heavily regulated exchange of information and the restrictions placed on the media, have created a one-of-a-kind programmatic landscape. Here, according to the whitepaper, are the four major models of programmatic ad buying.

1. Open exchange

The open exchange is a marketplace containing the lowest tier of publisher inventory that is sold via real-time bidding (RTB) at a low floor price. Typically, this inventory comes from small or medium-sized publishers, as the major publishers in China have their own exchanges.

In China, the biggest players on the open exchange are BES (Baidu Exchange Service), Tanx (Alibaba), GDT Adexchange (Tencent) and Doubleclick. They all connect to multiple DSPs and are flooded with inventory across small and medium publishers, making them very difficult to monitor.

The low quality of the inventory typically available on the open exchange results in poor brand safety, and so major advertisers generally avoid buying ads on these platforms. The association with the smaller brands that typically buy ads on open exchanges also contributes to this issue.

2. Private marketplace

The private marketplace, or PMP, is one step above the open exchange in the programmatic landscape. Only invited brands can take part in the auction, and the inventory is typically "more premium" than the open exchange, according to the report.

While the floor price is higher, the marketplace still uses RTB to ensure that the highest bidder wins the impression.

In China, the major PMP players are Sina AdX and Youku AdX.

Premium publishers have more leverage in China, and aim to be programmatic “one-stop shops.”

Their inventory is usually bundled with self-owned DSPs, so only invited independent DSPs (usually those with large buying volume) have access to inventory in these private exchanges, although they will occasionally release unsold remnant inventory to the open exchanges as well.

You might also like

- GroupM partners with Chinese data giants

- Yoyi Digital talks up 'Programmatic Plus'

- Marketing in China's unique digital ecosystem

3. Preferred deal

The inventory sold using the preferred deal model is of even higher quality than that sold on the private marketplace and the open exchange; basically, it is the top layer of inventory not sold directly.

Large advertisers will get the first look at this inventory before it released into a PMP. It is sold at a fixed CPM, but the volume is not guaranteed. This model is ideal for small to medium brands that want to buy high-quality inventory but have no traffic goals.

Due to the model’s non-guaranteed nature, it is also well-suited for big brands that want to maintain

a minimum level of activity between major campaigns.

While in Western markets, preferred deals are usually executed via third-party technology vendors, like Google’s PMP. However, Chinese publishers often bypass this step, endeavoring to offer the full

programmatic stack.

4. Programmatic premium

At the top of the programmatic pyramid lies programmatic premium. This model includes premium inventory directly purchased from the publisher at a higher fixed CPM and guaranteed volume. It carries the benefit of incremental reach without having to sacrifice the quality of the inventory.

In China, several differentiating factors make this model unique. One is that China has plenty of manual labor and therefore doesn’t fully embrace the purely automated model. In China, greater emphasis is placed on the “premium” aspect, because maintaining a relationship

with premium publishers remains very important.

Premium publishers are very cautious in opening up their inventory to DSPs, so the transaction takes on a mixed approach. The deal terms, price, and volume are specified offline, then an online system conducts the programmatic transaction.

Click image for larger view

China versus the world

The most obvious difference about China's ecosystem? Facebook, Google, YouTube and Yahoo are basically not part of it.

Plus, there is a lack of good third-party data and legal limitations on the freedom of information exchange has resulted in a lack of transparency.

Another major difference is the importance of business relationships in China. If an advertiser’s ad tech solution focuses primarily on premium inventory, they will need to build a good relationship with the publisher, as the top inventory won’t be released on the open exchange.

What are 'DSpans'?

Unlike the rest of the world, 'inventory neutrality' is not an issue for Chinese advertisers. Because of this, many DSPs operate their own ad networks—which traditionally purchase inventory from several publishers, bundle it and resell it at a higher cost—and mix these inventories into programmatic media selling to gain higher profit.

This unique hybrid model began with desktop display inventory and has now become very popular among mobile DSPs. RTBAsia coined the term DSpan to describe this model, a hybrid of DSP and ad networks.

A major problem with this model is the lack of neutrality. Typically, DSpans prioritise the sales of their own inventory first, above that of other publishers.

Challenges of programmatic in China

Advertisers in China have been slow to change their mindset from “content buying” to “audience buying.” They remain too accustomed to the cost-per-day system that allows them to clearly see where each ad is placed.

Another challenge is that China’s programmatic ecosystem remains incomplete. There are few third-party data management platforms, and this poses significant issues, creating a fragmented market in which exchanges interact with a plethora of demand- and supply-side platforms.

The confusing landscape makes fraud and transparency major issues that act as deterrents to the world’s top marketers due to concerns about brand safety.

How bad is fraud in China? Look out for part 2 of this report on CampaignAsia.com tomorrow.

(Editor's note, this piece has been largely drawn verbatim from R3 and RTBAsia's whitepaper, but edited and rearranged for clarity.)

.jpeg&h=334&w=500&q=100&v=20170226&c=1)

.jpg&h=334&w=500&q=100&v=20170226&c=1)

.png&h=334&w=500&q=100&v=20170226&c=1)

_23.jpg&h=268&w=401&q=100&v=20170226&c=1)

.jpg&h=268&w=401&q=100&v=20170226&c=1)